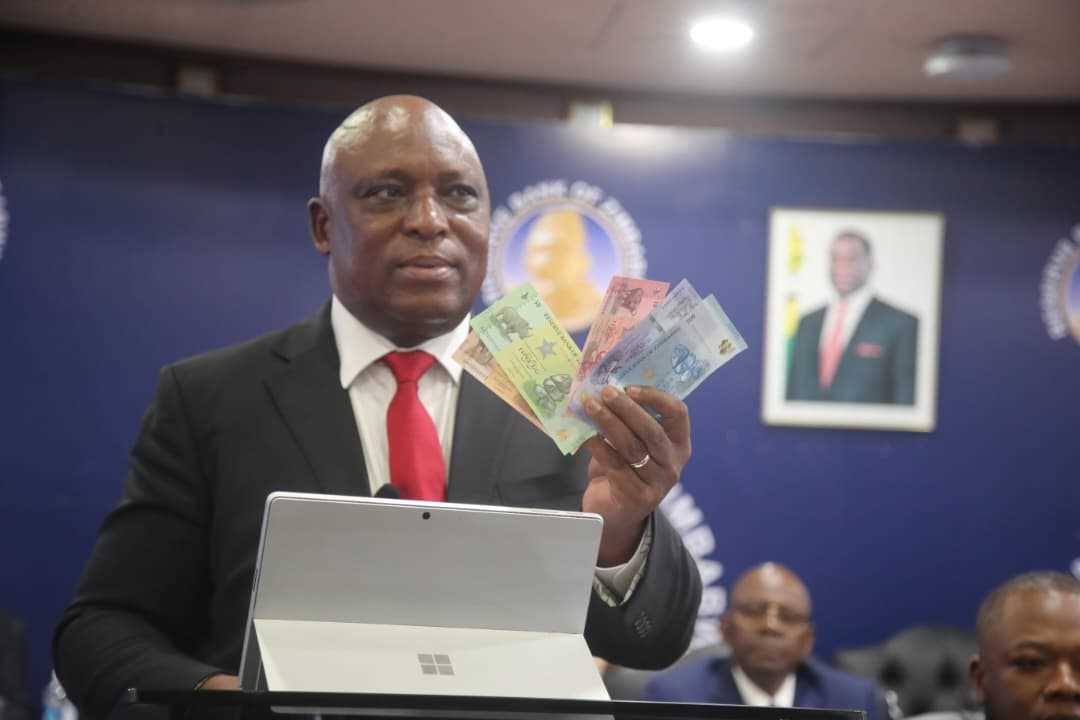

When the Reserve Bank of Zimbabwe unveiled the upgraded “Big Five” Zimbabwe Gold banknotes — ZiG10, ZiG20, ZiG50 and the upcoming ZiG100 and ZiG200 — the announcement was framed as part of a strategy to deepen domestic currency usage and strengthen monetary stability.

The notes will begin circulating on 7 April 2026, initially with the ZiG10, ZiG20 and ZiG50 denominations, while the higher denominations will follow later.

RBZ Governor John Mushayavanhu said the rollout represents a redesign of existing notes with improved security features and durability, adding that the new notes will circulate alongside the current ones.

Authorities insist the move will not increase the money supply because banks will simply convert electronic balances held at the central bank into physical cash.

The RBZ has also announced the reintroduction of ZiG coins to address the shortage of small change and prevent price distortions in everyday transactions.

But in Zimbabwe, the unveiling of larger banknotes has rarely been viewed as a neutral technical exercise. Historically, it has often been interpreted as a warning sign.

Zimbabwe’s monetary history is filled with moments when the introduction of larger denominations coincided with rising inflation and collapsing public confidence in the local currency. The pattern is so familiar that even the central bank itself previously acknowledged the psychological danger associated with larger notes.

In 2024, Mushayavanhu said the RBZ had deliberately avoided introducing higher denominations such as ZiG50 and ZiG200 because “psychologically, these denominations are inflationary.”

That caution now appears to have faded with the introduction of the “Big Five” series.

Zimbabwe’s currency story began very differently. When the Zimbabwe dollar was introduced in 1980 following independence, it was one of the strongest currencies in Africa, at times trading above the United States dollar. For nearly two decades, the system functioned relatively normally, although inflation gradually began to rise in the late 1990s as fiscal pressures and economic shocks intensified.

By the early 2000s, the country had entered a cycle that would become painfully familiar: prices began rising faster than wages, cash shortages emerged, and the central bank responded by printing progressively larger notes to keep transactions moving.

The escalation became extreme between 2006 and 2008, when Zimbabwe experienced one of the worst hyperinflation episodes in recorded economic history. Banknotes rapidly increased in value, moving from thousands to millions, then billions, and eventually trillion-dollar notes.

The appearance of each new denomination did not stabilise the system; it simply reflected the speed at which prices were rising.

By 2009, the Zimbabwe dollar had effectively collapsed, and the country abandoned it altogether, adopting a multi-currency system dominated by the US dollar.

The next phase of Zimbabwe’s monetary experimentation began cautiously. In 2014, the RBZ introduced bond coins to address the shortage of small change in a dollarised economy. Initially, the coins were tolerated because their value was low and they were backed by a facility intended to maintain parity with the US dollar.

But the situation changed when bond notes were introduced in 2016.

Authorities again insisted the notes were equivalent to the US dollar, but within months a parallel market exchange rate had emerged, reflecting declining public confidence.

In 2019, the government introduced the RTGS dollar, later renamed the Zimbabwe dollar. What followed was a rapid repetition of history. As inflation accelerated, larger denominations were introduced again, before the currency collapsed once more.

Related Stories

In April 2024, the government attempted a fresh reset with the introduction of Zimbabwe Gold (ZiG), a currency designed to be backed by gold and foreign currency reserves. Initially issued largely in electronic form, the currency was presented as a disciplined monetary system intended to break from the inflationary past.

For a time, the indicators appeared encouraging. The official exchange rate remained relatively stable around ZiG26 to ZiG27 per US dollar during 2025, while inflation slowed significantly.

More recently, the annual ZiG inflation rate for February 2026 was reported at 3.8%, down from 4.1% the previous month.

But stability in official statistics does not always translate into stability in the marketplace.

In Zimbabwe’s vast informal sector, which dominates everyday trade, exchange rates are determined less by official platforms and more by street-level purchasing power. In many transactions, ZiG20 is widely treated as roughly equivalent to about 50 US cents, implying an effective rate far weaker than the official market.

Such gaps between official exchange rates and informal market realities have historically been among the earliest indicators of declining currency confidence.

Another familiar casualty in this environment is small change.

Coins have rarely survived inflationary cycles in Zimbabwe. During previous currency regimes, coins were gradually pushed out of circulation as their purchasing power collapsed. Retailers stopped issuing them as change, consumers discarded them, and prices began rounding upward.

The RBZ’s plan to reintroduce ZiG coins therefore raises practical questions. Zimbabwe has never had a ZiG5 banknote, yet coins are expected to play a role in an economy where the smallest widely circulating note already begins at ZiG10.

If inflation expectations rise, coins may quickly lose their practical value, becoming symbolic currency rather than functional money.

This is where the psychological dimension of currency becomes important. Monetary systems are built not only on reserves and policy frameworks but also on trust. When larger banknotes appear, citizens often interpret them as a signal that prices will rise and the currency will weaken.

Zimbabwe’s economic memory amplifies this effect. The images of people carrying bags of banknotes, queuing for cash withdrawals, or watching salaries evaporate within days remain vivid in public consciousness.

Even the RBZ acknowledges that key conditions for a full transition to a mono-currency system have not yet been achieved.

Authorities say Zimbabwe still needs foreign currency reserves covering three to five months of imports — up from the current roughly one and a half months — along with sustained low inflation and a fully efficient foreign exchange market.

Until those conditions are met, confidence in the domestic currency remains fragile.

The unveiling of the ZiG “Big Five” series therefore arrives at a delicate moment. Inflation has been contained, the exchange rate has stabilised, and policymakers argue that macroeconomic fundamentals are improving.

Yet Zimbabwe’s monetary history has repeatedly followed a troubling pattern: stability emerges, larger denominations are introduced, inflation expectations shift, and the currency begins to weaken again.

This does not necessarily mean the cycle will repeat.

But Zimbabwe’s past has shown that bigger notes often appear not at the end of a currency crisis, but at the beginning of one.

And if history is any guide, the real test of the ZiG will not be the design of its banknotes, but whether Zimbabwe can finally break the cycle in which every new currency begins with hope, only to end buried under ever-larger pieces of paper.

Leave Comments