ZimNow Business Analysis Desk

Zimbabwe’s investment pipeline continues to swell on paper, but delivery on the ground tells a far leaner story, exposing a widening gap between approved projects and implementation.

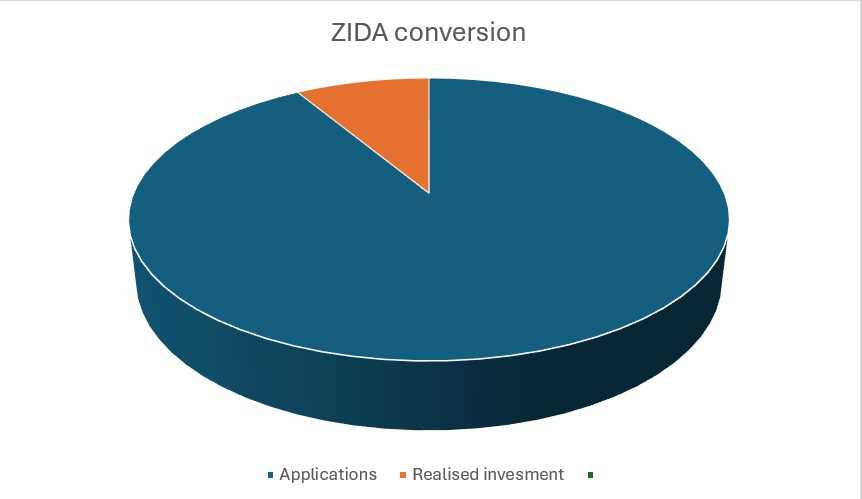

Recently reported data from the Zimbabwe Investment and Development Agency shows that while billions of dollars in investment commitments have been licensed in recent years, only a fraction is translating into real capital inflows and operational projects as large-scale projects dominate approvals, but many stall before execution.

The numbers at a glance

| Indicator | Value | What it means |

|---|---|---|

| Total projected investment (recent period) | US$52.968bn | Size of Zimbabwe’s approved pipeline |

| Actual realised investment | ~US$5bn (≈9%) | Conversion rate remains low |

| Q1 2026 projected investment | US$889m (3% of total) | Pipeline still growing |

| Q1 2026 realised investment | US$40m (≈5% of Q1) | Weak short-term conversion |

| Approved projects tracked | 3,611 | Large pipeline under monitoring |

| Projects with real progress | 18% | Majority not moving |

| Projects without implementation | 82% | Core execution problem |

| Manufacturing share | 32% (US$552m) | Leading sector |

| Energy sector realisation | US$723.7m | Strong interest, weak delivery |

| Harare + Mashonaland West share | 88% | Heavy geographic concentration |

| Remaining 7 provinces | 12% combined | Regional imbalance |

| Jobs projected (2026) | 3,817 | Modest employment impact |

| Share of national employment | 0.1% | Limited macro impact |

Projects with the largest ticket sizes, particularly in energy and mining-linked infrastructure, dominate the approvals list but lag in execution. Energy alone has attracted hundreds of millions in projected investment, yet realisation remains thin.

Manufacturing, often seen as a quicker win for industrialisation, leads in projected allocations but still reflects modest conversion into actual output.

ZIDA chief executive Tafadzwa Chinamo noted that monitoring reveals a large share of projects “approved but not implemented,” pointing to bottlenecks that extend beyond simple investor appetite.

Related Stories

Regulatory delays slowing project start times

Financing gaps, especially for capital-intensive projects

Shifts in investor sentiment mid-cycle

Infrastructure and input constraints

Chinamo has previously stressed that improving the “investment-to-delivery continuum” requires more than approvals, calling for tighter alignment between licensing, financing and implementation.

If capital is thin on the ground, it is even thinner outside the main corridors. Harare and Mashonaland West alone account for 88% of projected investment, largely driven by large industrial projects such as the Dinson Iron and Steel plant.

That leaves the remaining seven provinces sharing just 12%, with regions like Matabeleland North attracting less than 1% in some reporting periods.The result is a lopsided investment map, where national growth ambitions rest heavily on a few concentrated bets.

Despite billions in projected investment, job creation remains subdued. Formal jobs expected from these projects represent just 0.1% of Zimbabwe’s total employment.In other words, even if all currently tracked projects were delivered, the impact on unemployment would barely register at a national level.

Zimbabwe’s investment narrative is one of poor conversion. The country is attracting interest, signing deals and building a sizeable project pipeline. What is missing is consistent follow-through.

Leave Comments