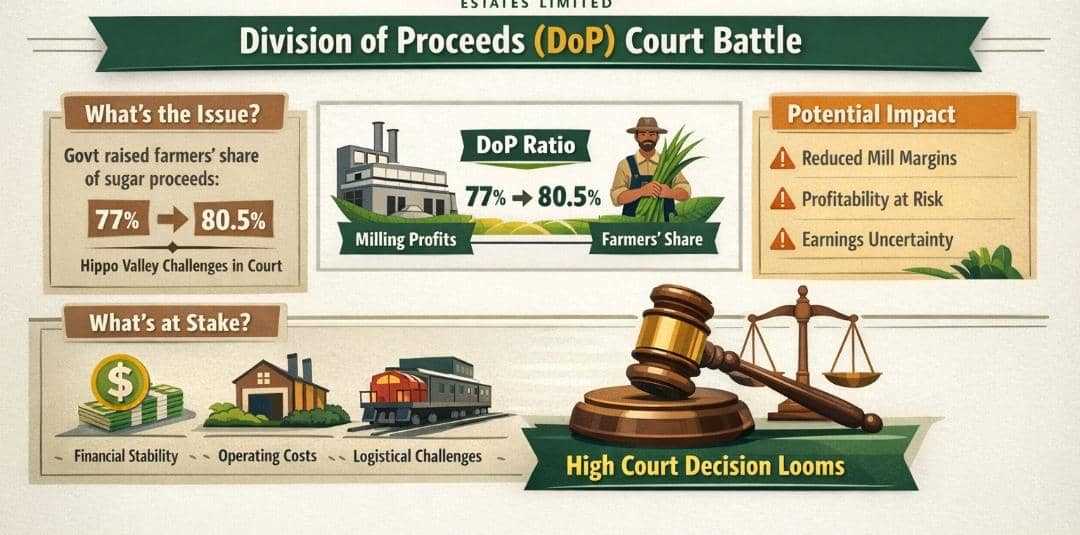

Hippo Valley Estates Limited’s otherwise solid half-year financial performance is now overshadowed by a High Court challenge that could materially alter the economics of its sugar milling business, after government moved to increase farmers’ share of proceeds under the Division of Proceeds framework.

In its interim results for the six months ended September 30, 2025, the Zimbabwe Stock Exchange-listed sugar producer reported stronger assets, higher production, and sharply improved operating profitability.

However, management has flagged the DoP dispute as a key uncertainty that could weigh heavily on future earnings should the court rule against the company.

“The determination by the Ministry of Industry and Commerce to revise the DoP ratio from 77 percent to 80.5 percent remains under legal challenge,” the company said in its interim report. “An adverse outcome could have a significant negative impact on the profitability of the milling business.”

Under the DoP model, revenue from sugar sales is split between millers and cane growers. While designed to balance interests across the value chain, Hippo Valley argues that the revised ratio threatens the sustainability of milling operations already under pressure from elevated input costs and infrastructure challenges.

Despite the legal headwinds, Hippo Valley delivered a resilient operational performance during the period. Sugar production rose 7 percent, while revenue increased 10 percent to US$112.9 million, supported by stronger local market sales volumes. Operating profit surged 79 percent to US$24.5 million, driven by efficiency gains under the company’s cost-reduction programme, Project Zambuko.

“Operational efficiencies and disciplined cost management continue to deliver tangible results,” management noted. “Project Zambuko remains central to positioning the business as a competitive, low-cost producer.”

Profit for the period, however, slipped marginally by 4 percent to US$17.5 million, largely due to a once-off tax credit recognised in the prior comparative period. Earnings per share were steady at 9 US cents.

Related Stories

The company’s balance sheet strengthened markedly, with total assets rising to US$209.1 million from US$173.0 million at the March 2025 year-end. Inventories almost doubled to US$77.8 million, reflecting a strong production season but also placing pressure on working capital. To support higher stock levels, borrowings increased, pushing total liabilities to US$95.1 million.

Cash generation was constrained by the inventory build-up, with net operating cash flows declining to US$2.9 million from US$7.2 million in the prior period. Hippo Valley drew on short-term funding to bridge seasonal liquidity requirements, resulting in a net financing inflow of US$4.3 million.

“In line with the seasonal nature of the business, short-term facilities were utilised to manage working capital during peak production,” the company said.

Given the legal uncertainty and ongoing capital demands, the board opted not to declare an interim dividend. Shareholder equity nonetheless grew to US$114.0 million, supported by profits generated during the period.

“The decision not to declare an interim dividend reflects a prudent approach to liquidity management and capital preservation,” the board said.

Beyond the DoP dispute, Hippo Valley continues to contend with structural cost pressures. Cane prices remain elevated at US$71 per tonne, well above regional averages, while inconsistent power supply, high electricity tariffs, rising labour costs, and global inflation in fertilisers and chemicals continue to erode margins.

Logistical bottlenecks, particularly inefficiencies at the National Railways of Zimbabwe, are also constraining export volumes. Management acknowledged that resolving these constraints is critical to unlocking value from regional and international markets.

Looking ahead, the company expects local demand for sugar to remain strong, supported by marketing initiatives around its Huletts brand. However, management was clear that the outcome of the DoP court challenge will be pivotal to the group’s medium-term outlook.

“The business remains a going concern with adequate water resources, a strong market position, and effective cost-control measures,” management said. “However, resolution of the DoP matter is critical to ensuring the long-term viability of milling operations.”

Leave Comments