Zimbabwe's annual inflation has remained below five percent for six consecutive months, giving the Reserve Bank of Zimbabwe (RBZ) greater confidence to begin easing monetary policy after nearly two years of maintaining one of Africa's highest interest rate regimes.

The central bank's decision to lower the Bank Policy Rate from 35 percent to 30 percent signals that policymakers increasingly believe the immediate threat of runaway inflation has receded. Yet the more important question is no longer whether inflation is falling, but whether improving macroeconomic indicators will translate into cheaper credit, stronger private sector investment and higher living standards.

The RBZ's Quarter Two 2026 Snapshot on Recent Monetary, Currency, Price and Financial Developments shows annual Zimbabwe Gold inflation stood at 4.7 percent at the end of June, while month-on-month inflation averaged just 0.47 percent during the first half of the year.

Reserve Bank Governor John Mushayavanhu attributed the outcome to a combination of tight monetary policy and government interventions, particularly in cushioning the economy from higher global fuel prices following the Middle East oil shock.

"The prudent monetary policy stance, coupled with proactive government interventions in the fuel sector, have helped the country to weather the inflationary impact of the recent oil price shock from the Middle East crisis as reflected by annual inflation which remained below 5% since January 2026," he said.

The Monetary Policy Committee subsequently reduced the policy rate to 30 percent after concluding that Zimbabwe had moved from a high-inflation environment to one characterised by relative price stability.

"The Reserve Bank will continue to calibrate the monetary policy stance in line with the evolution of macroeconomic fundamentals to support the country's inflation and growth objectives," Mushayavanhu said.

The central bank also lowered the Targeted Finance Facility interest rate from 20 percent to 15 percent while maintaining a lending cap of 25 percent for productive sector financing.

The policy shift represents an important change in the RBZ's priorities. For much of the past two years, monetary policy focused primarily on containing inflation and stabilising the Zimbabwe Gold currency, even at the cost of expensive borrowing. With inflation now broadly contained, the challenge is increasingly becoming how to support economic expansion without reigniting price pressures.

Whether the rate cuts will stimulate economic activity, however, remains uncertain.

At 30 percent, Zimbabwe's benchmark interest rate remains exceptionally high by regional standards. Commercial banks typically price loans well above the policy rate, meaning borrowing costs may still remain beyond the reach of many businesses, particularly small and medium-sized enterprises that have consistently identified access to affordable finance as one of their biggest constraints.

Lower inflation also does not automatically translate into improved household welfare.

Related Stories

Inflation measures the pace at which prices increase rather than the level of prices themselves. Although prices are rising more slowly, households continue to absorb the cumulative impact of previous inflation episodes alongside stagnant incomes and persistently high costs of food, transport, housing and other essentials. Without stronger income growth, many consumers may experience little immediate improvement in purchasing power despite the more stable inflation environment.

The broader monetary indicators nevertheless point to increasing stability within the financial system.

Zimbabwe Gold deposits increased from ZiG21.5 billion in March to ZiG26.9 billion in June, suggesting growing use of the local currency within the banking sector. Reserve money rose to ZiG6.6 billion while remaining within targets agreed under Zimbabwe's International Monetary Fund Staff-Monitored Programme, indicating that liquidity expansion has remained relatively controlled.

External sector indicators also strengthened.

Foreign currency receipts reached US$10.72 billion during the first half of 2026, up from US$7.25 billion during the same period last year. Gross foreign currency reserves increased to US$1.6 billion, equivalent to approximately 1.6 months of import cover, while reserves backing the Zimbabwe Gold currency stood at roughly six times reserve money, reinforcing the RBZ's argument that the local currency remains adequately supported.

Exchange rate stability has also improved considerably.

The Zimbabwe Gold traded within a relatively narrow range of ZiG26.5 to ZiG27 per US dollar during the quarter. Although the RBZ acknowledged that the premium between the official and parallel markets remained below 20 percent, the persistence of that gap suggests some businesses and consumers still place greater confidence in the informal foreign exchange market than the official system.

Meanwhile, the report shows Zimbabwe Gold accounted for around 40 percent of national payment system transactions, indicating growing domestic acceptance of the currency even though the US dollar continues to dominate significant parts of the economy.

Other financial stability indicators also remained positive, with the banking sector's non-performing loan ratio at 3.64 percent and Zimbabwe recording a current account surplus of more than US$570 million during the period.

The RBZ argues that these trends demonstrate increasing confidence in both the financial system and the local currency.

That assessment broadly aligns with recent observations by the International Monetary Fund, which has acknowledged improvements in fiscal discipline, inflation management and exchange rate stability under Zimbabwe's Staff-Monitored Programme. However, the IMF has also cautioned that maintaining those gains will require continued policy consistency and structural reforms while warning that commodity price volatility and climate-related shocks remain significant risks to the economy.

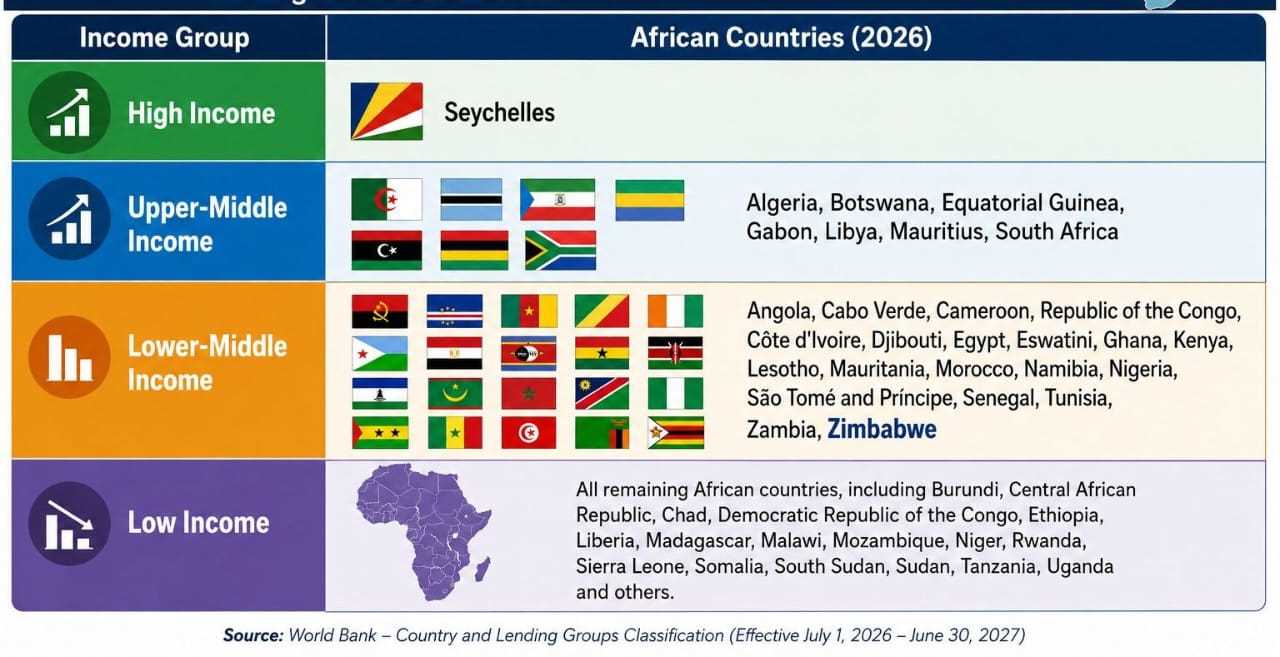

As Zimbabwe pursues its ambition of attaining upper-middle-income status, the sustainability of these gains will increasingly be judged less by inflation statistics and more by their impact on the productive economy.

The real test of the RBZ's policy shift will be whether commercial banks extend more affordable credit, businesses respond with higher investment, formal employment expands, real wages recover and households begin to experience tangible improvements in purchasing power. Until those outcomes materialise, the recent improvement in macroeconomic indicators, while significant, will remain only the first stage of Zimbabwe's broader economic recovery.

Leave Comments