The Chinese Embassy's careful statement to its firms in Zimbabwe, warning of 'investment and operational risks' reveals far more about the state of the Harare-Beijing relationship than it appears to on the surface.

When the Chinese Embassy in Harare released a statement this week telling Chinese enterprises to 'strengthen risk prevention and compliance awareness' following Zimbabwe's sudden lithium export ban, the diplomatic phrasing was almost too polished to be accidental.

Reading between the lines, this was a carefully calibrated signal, directed simultaneously at Chinese investors, the Zimbabwean government, and Beijing's own domestic audience.

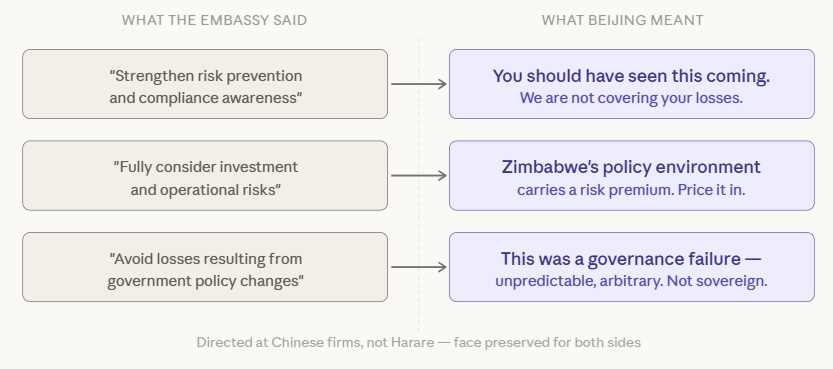

The statement advised investors to 'fully consider various investment and operational risks and make informed decisions so as to avoid losses resulting from government policy changes.' Translated from diplomatic language: Beijing was putting Harare on notice that the abrupt, no-warning nature of this ban was not acceptable conduct between partners, without ever saying so directly. And warning any Chinese players considering working with Zimbabwe, at any level, that they must be prepared to risk a volatile operating environment.

More Than a Mining Policy

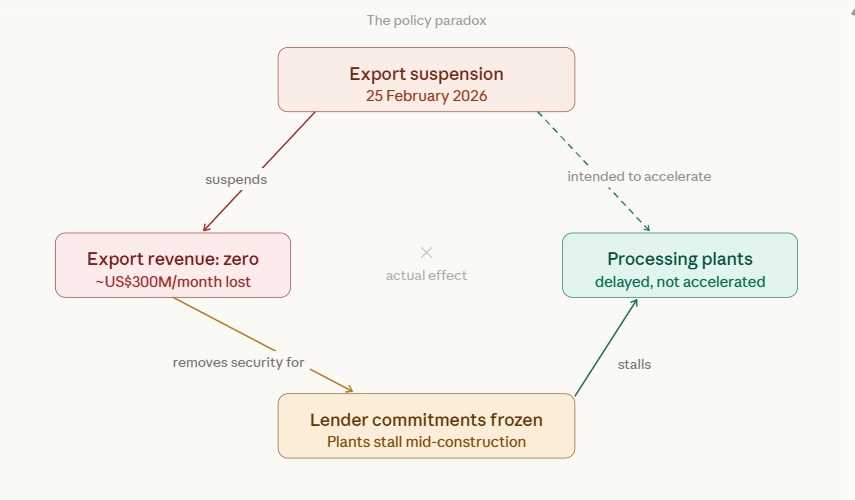

Zimbabwe's Mines Minister Polite Kambamura announced the suspension of all raw mineral and lithium concentrate exports on 25 February 2026, with immediate effect, including shipments already in transit. The move accelerated a ban that had been scheduled for January 2027, advancing it by nearly a year with no prior consultation period.

The official rationale centred on 'malpractices and leakages' in the export chain. But the economic logic runs deeper. Despite Zimbabwe exporting over 1.1 million metric tonnes of spodumene concentrate in 2025, an 11% year-on-year increase, export revenues actually fell slightly, dropping from roughly US$514.5 million in 2024 to US$513.8 million. Zimbabwe was producing more and earning less. The structural problem was visible to anyone paying attention.

What those export revenue figures do not capture is the depth of investment that Chinese-backed firms had already committed to on the ground. The five principal producers, Bikita Minerals, Prospect Lithium Zimbabwe, Kamativi Mining Company, Gwanda Lithium, and Sabi Star, subsidiaries and joint ventures of Sinomine Resource Group, Huayou Cobalt, Yahua Group, Tsingshan Holding Group, and Chengxin Lithium Group respectively, collectively deployed over US$1.1 billion into Zimbabwe's lithium economy between 2022 and 2025. They did this during one of the most severe global lithium price downturns on record. That counter-cyclical commitment speaks to how strategically these companies regard their Zimbabwean positions, and why the abruptness of the ban landed as it did in Beijing.

In that context, the export ban is less a protectionist reflex and more a belated assertion of commodity sovereignty, a playbook being run with increasing confidence across resource-rich African states from the DRC to Namibia.

The question is where this leaves Zimbabwe's all-weather partnership with Beijing.

Diplomatic Rebuke in Polite Clothing

Beijing's response has been notable. There was no formal diplomatic protest, at least in the public domain. No threat of reduced investment flows.

Instead, the Chinese Embassy issued a statement framed as guidance to its own business community. This framing is deliberate. By directing the rebuke inward, at Chinese firms rather than at the Zimbabwean government Beijing preserved face for both sides.

The statement cannot be read as interference in Zimbabwe's internal affairs. But its meaning should be unmistakable to anyone in Harare who understands how Chinese diplomatic communication works.

The phrase 'avoid losses resulting from government policy changes' is the key tell. It implicitly codes the ban as a governance failure — an unpredictable, arbitrary policy shift — rather than as a legitimate sovereign decision.

In the same breath, it signals to Chinese investors that they should not have been caught off-guard by this, and that the business environment in Zimbabwe carries a risk premium that they need to price into future decisions.

This is an unusually pointed message from Beijing. The two countries have enjoyed what is routinely described as a 'comprehensive strategic partnership,' cemented through the Look East policy era and deepened through over US$1.4 billion in Chinese lithium investment since 2021. Public friction is rare.

The embassy's decision to issue this statement at all reflects genuine concern at the policy process, even if the language is calibrated to keep overt irritation off the front page.

The Market Numbers Tell the Real Story of Chinese Exposure

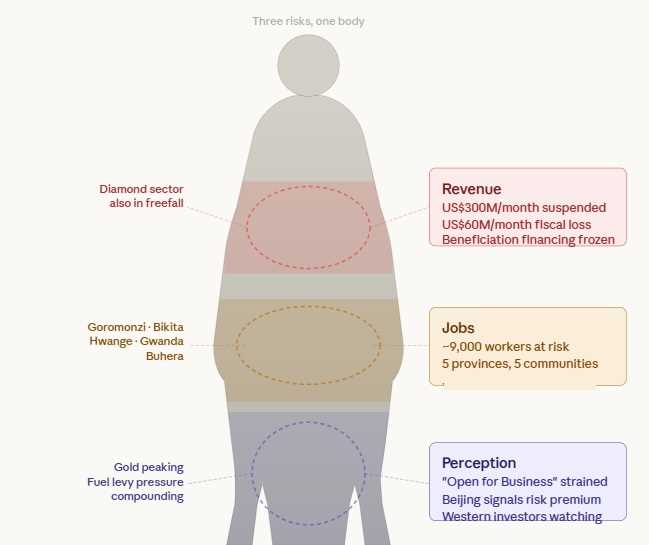

To understand why Beijing responded at all, consider the scale of Chinese exposure. The five affected companies alone had deployed over US$1.1 billion into the sector and were generating approximately US$300 million per month in export revenues prior to the suspension — revenues that supported not only their own operations but an estimated US$60 million per month in Zimbabwean fiscal receipts in the form of royalties, taxes, and levies. When that income line was severed on 25 February, it did not merely affect company balance sheets. It removed a significant and recurring source of government revenue.

Related Stories

China sourced roughly 15–19% of its total lithium feedstock from Zimbabwe in 2025. When Zimbabwe suspended exports, Chinese lithium carbonate futures on the Guangzhou exchange moved sharply upward within hours, with intraday swings of 5–9% recorded on 26 February.

These firms built their Zimbabwean operations around a vertically integrated model: mine the spodumene in Zimbabwe, ship the concentrate to China, process it into battery-grade lithium there. The ban severs that model at the wrist.

The scale of what is now at stake domestically gives texture to Beijing's alarm. Across the five operations, approximately 9,000 Zimbabweans are employed directly and indirectly — communities in Goromonzi, Bikita, Hwange, Gwanda, and Buhera, spanning five of Zimbabwe's provinces. The producers have built over 100 kilometres of roads, installed solar-powered community boreholes, and extended high-voltage power infrastructure into areas that previously had none. The export ban has not merely paused a business. It has placed a national footprint on hold.

Huayou's US$400 million lithium sulphate plant, commissioned in Zimbabwe in October 2025, is suddenly far more central to the operating model than it was designed to be. Sinomine's planned US$500 million sulphate plant at Bikita now looks prescient but also more urgently necessary. The ban has, in effect, force-multiplied Chinese firms' incentive to invest in in-country processing — which is precisely what Zimbabwe's government has been demanding for years. The irony is that the policy achieved through coercion what years of negotiation did not.

There is, however, a structural paradox embedded in this outcome. The lithium sulfate processing plants that the ban is designed to accelerate depend on capital — and that capital has historically been raised against contracted export revenue streams. The producers report that lenders financing beneficiation plant construction have now suspended their commitments, pending clarity on the revenue position. The export suspension has therefore interrupted the very financing mechanism through which processing infrastructure was being built. Whether that circle can be squared, and how quickly, is perhaps the most important practical question in this standoff.

What This Means for the Zim-China Relationship

The short answer is: it will survive. The relationship is structurally durable because both sides need it. Zimbabwe has few alternative partners of comparable scale willing to absorb its commodity exports and provide capital on non-conditionality terms. China has enormous sunk costs in Zimbabwean lithium infrastructure and cannot easily substitute Zimbabwean supply at volume.

But the dynamic has shifted. Zimbabwe's heavy dependence on Chinese capital arose from a context of Western sanctions and limited market access. Now the West, notably the US, is circling. US Ambassador Pamela Tremont recently stated outright that the country is interested in exploiting Zimbabwe's green energy resources.

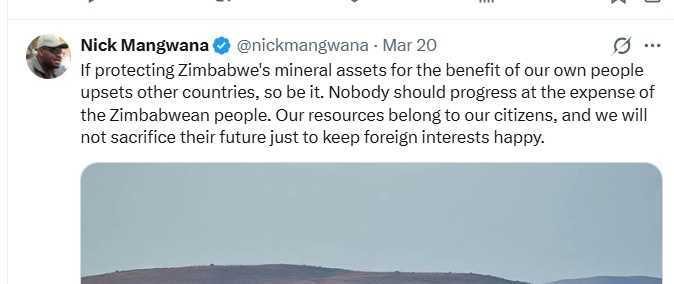

The export ban suggests that the Mnangagwa administration has calculated that with global demand for lithium rising and Zimbabwe holding Africa's largest reserves, the country is in a powerful enough position to begin setting terms. The Chinese Embassy's statement suggests Beijing does not necessarily reject Zimbabwe's resource nationalism, but would have preferred bilateral discussions before announcement.

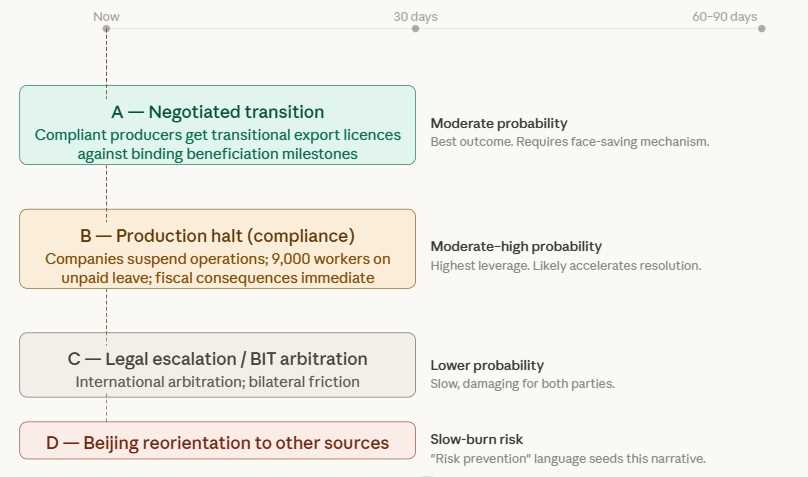

Three Scenarios to Watch

The next 60-90 days will be revealing. Three trajectories are plausible.

The first is rapid accommodation: Chinese firms already holding approved processing plants or near-completion facilities are probably seeking exemptions or fast-track approvals from the Zimbabwean government, effectively accepting the new beneficiation terms. This outcome suits both sides and is the most likely near-term path for Huayou and Sinomine, who have invested too heavily to walk away.

The second is quiet pressure: Beijing uses diplomatic channels and debt leverage , Zimbabwe's significant Chinese loan obligations, to push for a modified implementation of the ban that grandfathers existing supply agreements or creates a phase-in window. This is consistent with the embassy statement's tone and represents China using the tools available to it without escalating publicly.

The third, and most consequential, is reorientation: a gradual Chinese signal that Zimbabwe's governance risk makes it a less preferred minerals partner relative to peers, with investment flows to Chilean brine or Australian spodumene accelerating as hedges. This would be a slow-burn consequence rather than an immediate reaction, but the embassy's 'risk prevention' language is the first seed of that narrative.tu

A fourth possibility, less discussed, is that the industry itself moves first. If the affected producers determine that they cannot sustain operations, paying approximately 9,000 workers across five provinces on zero export revenues, servicing debt facilities structured against contracts now in default, maintaining sites whose concentrate stockpiles are accumulating with no route to market — a coordinated and orderly production suspension becomes not a threat but an operational inevitability. That outcome would make the fiscal consequences of the ban immediate and undeniable, and would almost certainly accelerate a government response. Whether that response takes the form of a negotiated transitional framework or a hardening of positions remains the open question.

The Bottom Line

Zimbabwe's lithium export ban is an act of economic self-assertion that was almost certainly overdue. The Chinese Embassy's response carefully worded, diplomatically contained, but pointed in its implications, says that Beijing feels there was a better way of handling the issue.

The 'all-weather friendship' between Harare and Beijing is entering a new phase. Zimbabwe has opened a new chapter in that relationship as it moves from words to action on becoming a processing nation, not merely an extraction one. The stance from the government appears to be a hardlining one.

But banning lithium exports in itself is not enough. The structural arithmetic is unforgiving: the US$300 million monthly revenue stream that has been suspended was not merely company income. It was the financing backbone for the processing infrastructure the ban was designed to create. Government has to work towards building a viable processing environment alongside the policy — affordable and efficient power supply, working rail infrastructure, strong governance systems, real anti-corruption mechanisms, and currency stability. These challenges to operational efficiency will not automatically go away as a result of the ban.

The policy has created the incentive for beneficiation. What it has not yet created is the conditions.

For now, the Zimbabwe Investment and Development Authority reports are the figures to watch. Will we continue to see China dominate the licence lists? And if Chinese investor inflows fall off, will we see a corresponding rise in Western investors picking up the slack?

Or will Beijing's pain send a message that is received globally?

Leave Comments