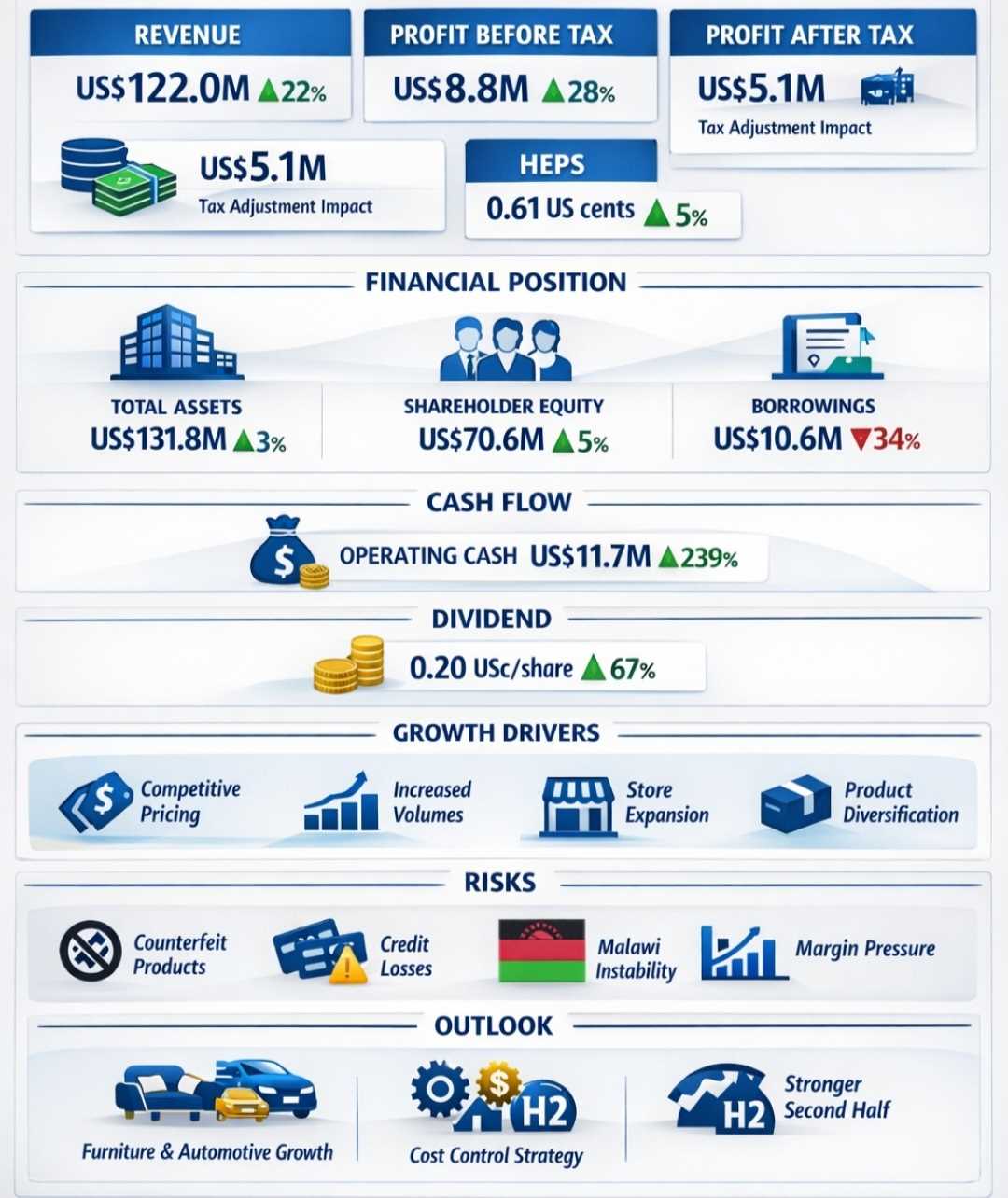

Axia Corporation Limited delivered a strong financial performance for the half year ended December 31, 2025, with revenue surging 22% to US$122 million, driven by increased volumes and competitive pricing across its business units.

The retail and distribution group also recorded a 28% rise in profit before tax to US$8.8 million, reflecting robust trading during the period. However, profit after tax marginally declined to US$5.1 million due to a once-off tax adjustment linked to prior financial periods.

The company said underlying performance remained solid, with headline earnings per share increasing by 5% to 0.61 US cents.

A key highlight of the period was Axia’s strengthened balance sheet, as the group reduced total borrowings by 34% to US$10.6 million as part of its deleveraging strategy. Total assets rose 3% to US$131.8 million, while shareholder equity increased 5% to US$70.6 million.

The group also reported exceptional cash generation, with net cash from operating activities jumping 239% to US$11.7 million, underlining strong working capital management and improved trading efficiencies.

Management attributed the performance to a relatively stable operating environment and improved access to foreign currency.

“A largely stable Zimbabwean trading environment, coupled with improved US dollar liquidity, provided a solid foundation for growth,” the company said.

Related Stories

The group added that its strategy centred on competitive pricing, store expansion and product diversification had driven record turnover during key promotional periods.

“The Group’s strategy of competitive pricing, expanding its store network, and enhancing its product range has yielded record turnover in key promotions,” management noted.

During the period, Axia declared an interim dividend of 0.20 US cents per share, representing a 67% increase from the prior period, signalling confidence in its financial position and future prospects.

Despite the strong performance, the group flagged several risks, including the proliferation of counterfeit products, which continue to erode margins for formal retailers, and rising credit risk within its distribution segment.

A tax provision of US$1.017 million at subsidiary TV Sales & Home, following an assessment by the Zimbabwe Revenue Authority, also weighed on net earnings for the period, although the company stressed this was a non-recurring item.

Looking ahead, Axia said it remains focused on driving growth in its core furniture and automotive segments, while maintaining cost discipline and improving operational efficiencies.

“By managing costs, pursuing growth in the furniture and automotive sectors, and leveraging its strong market position, the Group is well-positioned for a stronger performance in the second half of the financial year,” management said.

However, regional headwinds persist, particularly in Malawi, where high inflation and foreign currency shortages continue to pose operational challenges.

Leave Comments