The Ministry of Finance has moved to clarify the scope and intent of Zimbabwe’s newly introduced Digital Services Withholding Tax following confusion over its application to international payments, directing the Zimbabwe Revenue Authority to implement the measure strictly in line with policy intention.

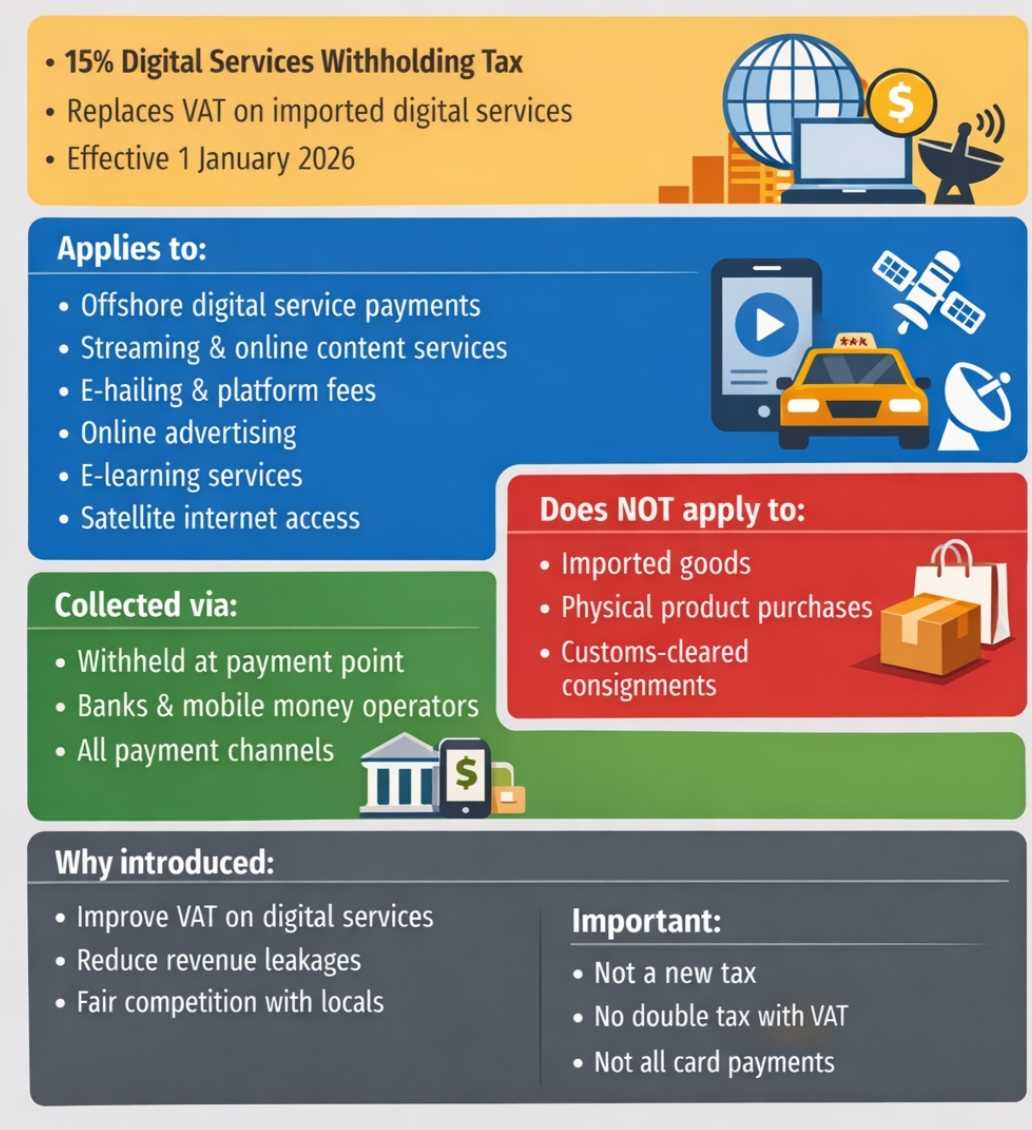

The DSWT was introduced through the 2025 National Budget and came into effect on 1 January 2026.

Finance Minister Mthuli Ncube announced the measure as part of efforts to strengthen the tax system and bring income earned by offshore digital platforms into the tax net.

“I therefore propose to introduce a Digital Services Withholding Tax at a rate of 15 percent, in lieu of VAT on imported services, for payments made to offshore digital platforms, including e-hailing fees, online content charges and satellite-based internet access fees,” Ncube said in his budget statement.

The tax is designed as an alternative collection mechanism for Value Added Tax on imported digital services, addressing long-standing challenges in taxing offshore service providers with no physical presence in Zimbabwe. Treasury has stressed that the DSWT is not a new tax, but an administrative tool to improve compliance.

“Imported services have been chargeable to VAT since the introduction of VAT legislation in 2004,” the Ministry said in a press statement dated 7 January 2026.

“The DSWT was introduced to improve collection of VAT on imported services, and not as an additional tax.”

However, confusion arose following the promulgation of Finance Act No. 7 of 2025, which incorrectly suggested that the withholding tax applied to all imported goods and services. In a letter dated January 5, 2026 to ZIMRA Commissioner-General Regina Chinamasa, Treasury acknowledged the error and issued corrective guidance.

Related Stories

“The tax should, however, be applied on imported services only, while VAT on imported goods will be chargeable at the time a consignment is cleared into the country,” the Ministry stated, directing ZIMRA “to implement the tax in line with the policy intention.”

Treasury further clarified that the DSWT applies exclusively to payments made to non-resident suppliers for imported digital services, including streaming platforms, online advertising, e-learning services, platform-based fees and satellite-based internet access.

The online purchase of goods, even when paid for through international platforms, does not fall under the scope of the tax and remains subject to existing customs duty and VAT at the point of importation.

To facilitate collection, banks, mobile money operators and other regulated payment intermediaries have been mandated to withhold and remit the tax at the point of payment.

According to the Minister, this approach ensures “efficient and real-time collection of revenue,” while also reducing leakages associated with offshore payments.

Treasury also cautioned financial institutions against applying the tax indiscriminately to all international card transactions.

“The Ministry has noted communication suggesting that the tax applies uniformly to all international card transactions irrespective of the underlying supply,” the statement said. “This interpretation is inconsistent with the policy or legislative intent.”

Engagements with banks and payment processors are ongoing, with ZIMRA expected to issue detailed administrative and operational guidelines to ensure consistent application of the tax. Financial institutions have also been instructed to immediately advise withholding agents of the corrected scope of the measure.

“These measures are necessary to safeguard the country’s tax base, promote equity in the tax system, and modernise revenue administration in line with the digitalisation of the economy,” Treasury said.

The DSWT applies at a rate of 15 percent, in lieu of VAT on imported services, while the qualifying threshold for the 5 percent Electronic Commerce Operators’ Tax has also been removed with effect from January 1, 2026.

Leave Comments