Econet Wireless Zimbabwe Limited’s decision to pursue a voluntary delisting from the Zimbabwe Stock Exchange after 27 years as a listed company marks one of the most consequential corporate actions in the market’s recent history, with implications extending well beyond the telecommunications sector.

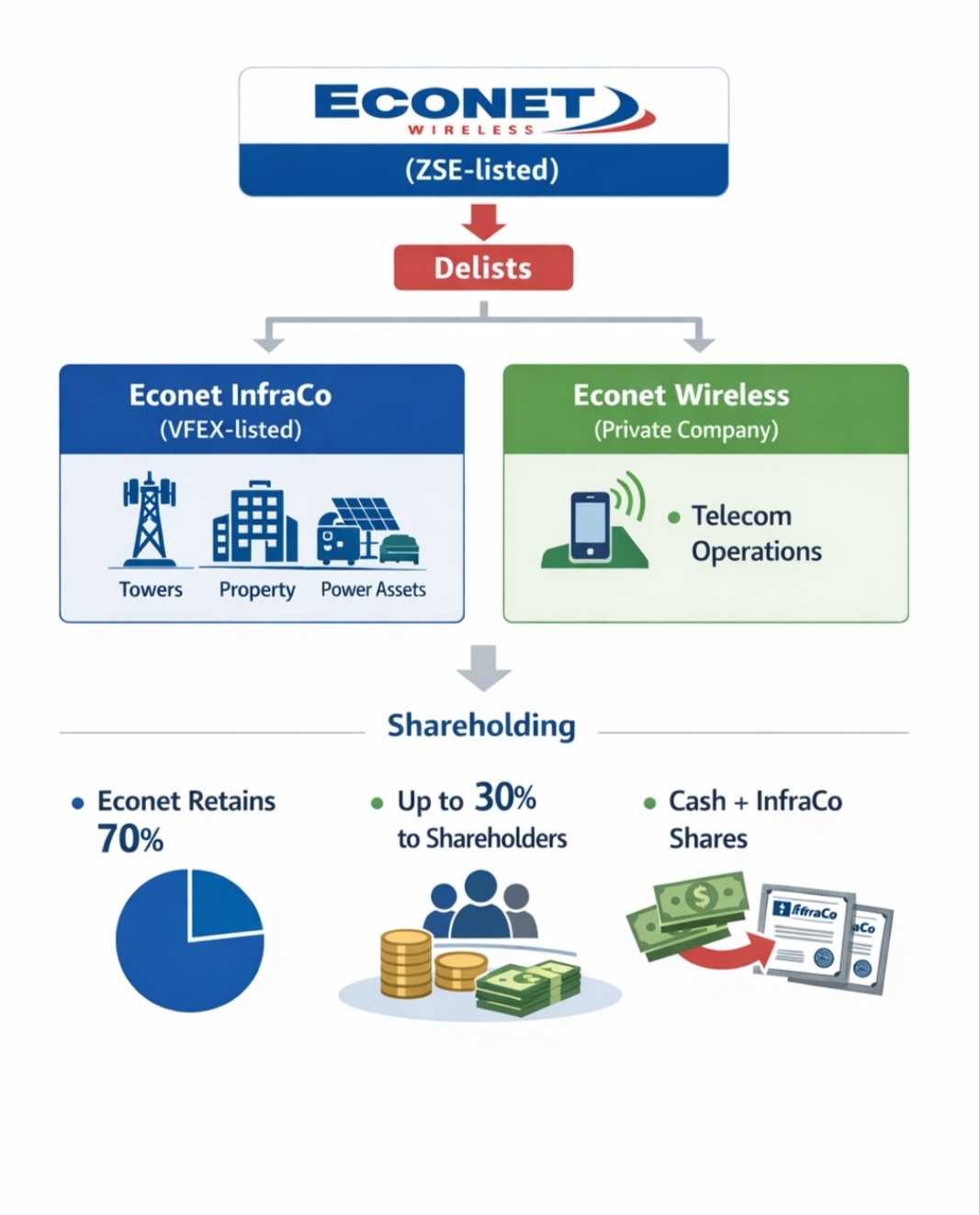

The proposed transaction involves the separation of Econet’s passive infrastructure assets into a newly formed entity, Econet Infrastructure Company Limited (Econet InfraCo), which is intended to be listed on the Victoria Falls Stock Exchange.

Econet Wireless Zimbabwe, stripped of these hard assets, would continue operating as a privately held company, subject to shareholder approval.

The board has cited persistent undervaluation on the ZSE, limited liquidity and the inability to realise fair value for infrastructure assets as the primary motivations behind the move.

How the Structure Works

Under the proposed arrangement, Econet InfraCo will house the Group’s towers, real estate and power assets, including sites supporting 2G, 3G, LTE and 5G networks, as well as energy infrastructure such as solar installations, battery systems and generators.

Econet Wireless Zimbabwe will retain a 70 percent stake in InfraCo, while up to 30 percent of InfraCo shares will be distributed to existing Econet shareholders as part of a voluntary exit offer. That offer will be settled partly in cash and partly in InfraCo shares, with the precise cash proportion yet to be disclosed.

InfraCo is expected to list on the VFEX by way of introduction, a mechanism that does not raise new capital but allows existing shares to be traded on the exchange.

Shareholders who decline the exit offer will remain invested in Econet Wireless Zimbabwe as an unlisted company, subject to private share transfers and reinstated pre-emption rights under company law.

The Valuation Argument

In its cautionary announcement, the board pointed to valuation multiples across African telecommunications peers, noting that operators trading at between six and eight times EV/EBITDA have typically separated and monetised their passive infrastructure through tower companies.

Econet argues that retaining infrastructure within the operating company has contributed to the market discount applied to its shares on the ZSE. By contrast, the VFEX, which operates in US dollars and has attracted property and infrastructure listings, is viewed by the board as a more suitable platform for valuing long-life infrastructure assets.

An independent expert is expected to determine the valuation of Econet InfraCo shares to be used in settling the exit offer.

Minority Shareholder Considerations

While the proposal has been framed as a value-unlocking exercise, it has brought governance and disclosure issues into sharper focus, particularly for minority shareholders.

The exit offer has not yet specified the percentage to be settled in cash, the currency of settlement or the funding source for the cash component. InfraCo shares, while listed, will initially represent an investment in a newly introduced security whose trading liquidity remains untested.

For shareholders who remain invested post-delisting, Econet Wireless Zimbabwe shares will no longer benefit from public price discovery, daily liquidity or the regulatory protections of a listed environment.

These dynamics redistribute liquidity and holding-period risk, raising questions about how minority interests are safeguarded during the transition from a public to a private structure.

Related Stories

The Liquid Question

Another aspect attracting scrutiny is the position of Liquid Intelligent Technologies within the wider Econet Group.

Liquid is a pan-African digital infrastructure business with fibre networks, data centres and cloud platforms operating across multiple jurisdictions and generating predominantly US dollar revenues. In functional terms, it already operates as an infrastructure business, albeit focused on digital rather than passive physical assets.

Liquid does not feature in the current value-unlock narrative, nor does it form part of the exit-offer mechanism. This distinction underscores a strategic separation between offshore, USD-earning digital infrastructure and domestically based passive assets, while also highlighting the selective nature of the asset carve-out underpinning the transaction.

“The decision to create a separate Zimbabwe-based InfraCo housing towers, real estate and power assets, and to use that entity rather than existing infrastructure assets to settle minority exits, suggests a selective asset carve-out rather than a holistic value-unlock,” a capital markets commentator said.

Market-Wide Implications

Econet’s potential exit represents a significant blow to the ZSE. The company accounts for roughly a third of the exchange’s total market capitalisation and is among its most actively traded stocks, attracting both institutional and retail investors.

Its departure would materially reduce daily trading volumes, weaken market depth and further concentrate liquidity in a shrinking pool of listed companies. The move follows earlier delistings by Powerspeed Electrical and the planned exit of National Tyre Services, reinforcing concerns about the ZSE’s ability to retain large, asset-heavy issuers.

Market participants warn that Econet’s decision should be viewed as a systemic signal rather than an isolated corporate restructuring, reflecting deeper challenges around currency risk, valuation confidence and capital formation in Zimbabwe’s domestic equity market.

Waison Makumbirofa, Chief Finance Officer at Microchannel Zimbabwe, said: “This should be treated as a systemic warning, not an isolated corporate action. The ZSE and policymakers need to move quickly and decisively to address the underlying issues.

Without real reforms, this risks becoming the beginning of a dam break, where confidence erosion accelerates further exits.

Capital markets run on trust. Once that trust fractures, restoring it becomes far harder than preventing the damage in the first place.”

Shareholding Structure

Econet Wireless Zimbabwe’s shareholder base is dominated by strategic and institutional investors.

Econet Global Limited holds approximately 42.9 percent of the issued shares, followed by Econet Wireless Zimbabwe SPV Limited with 4.6 percent. Old Mutual Life Assurance Company (Zimbabwe) owns 3.5 percent, New Arx Trust 3.3 percent and Makomo Engineering just over 2 percent. Other shareholders include Austin Eco Holdings, Mega Market, Allan Gray and VanEck Associates.

The concentration of ownership means minority shareholders’ voting and economic decisions will be central to the outcome of the proposed delisting.

A Defining Moment

If approved, Econet’s exit would mark the end of one of the ZSE’s longest-running and most influential listings. More broadly, it would reinforce the growing divergence between Zimbabwe’s local-currency equity market and the US dollar-based VFEX, where exporters and infrastructure assets increasingly seek refuge.

For now, the board has urged caution until further details are released. The market, however, is already treating the announcement as a watershed moment.

Leave Comments