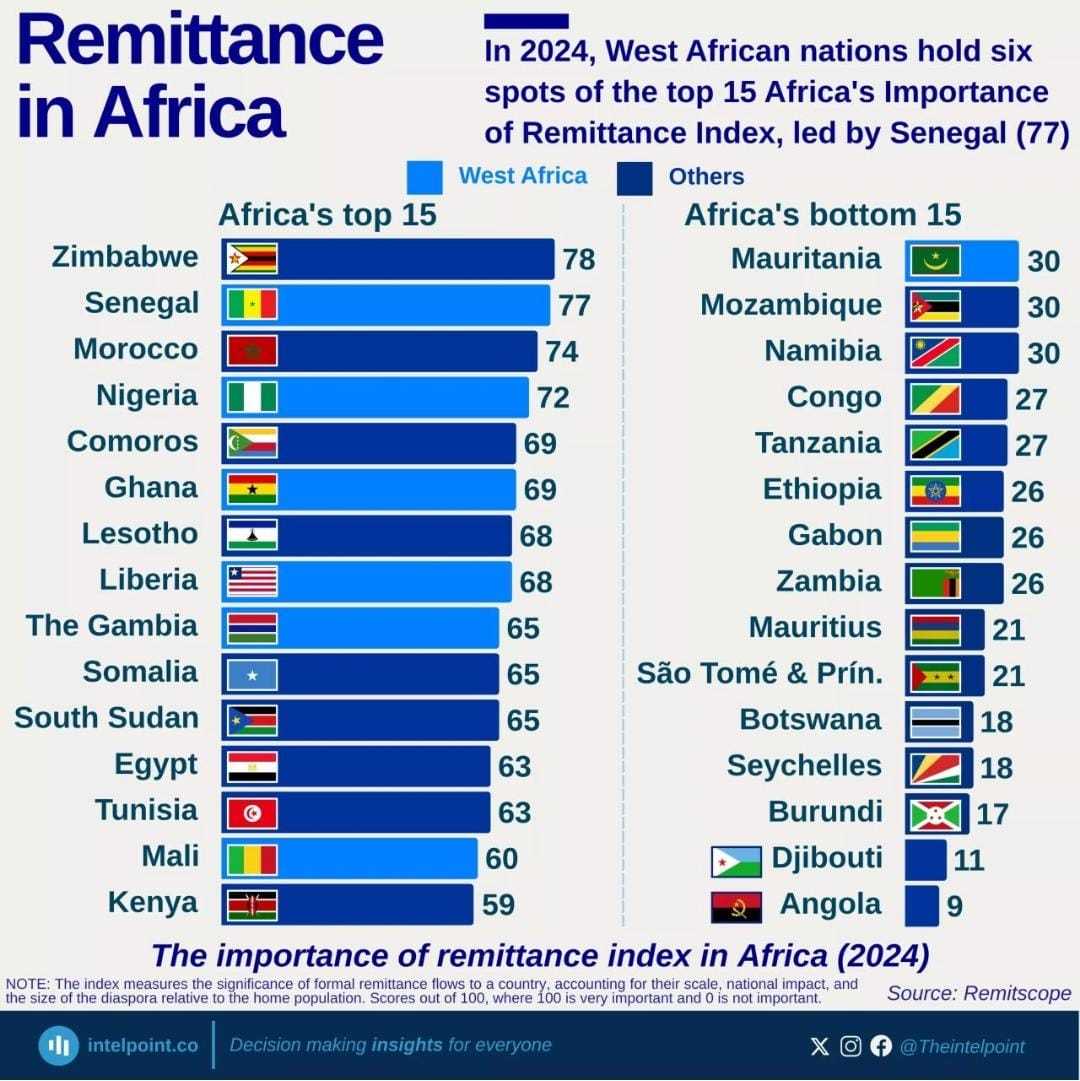

Zimbabwe has emerged as Africa’s most remittance-dependent economy after topping the 2024 Importance of Remittance Index, a development that highlights both the strength of diaspora support and the country’s failure to convert inflows into long-term economic investment.

According to the 2024 index compiled by Remitscope, Zimbabwe ranked first on the continent with a score of 78, ahead of Senegal at 77 and Morocco at 74. The index evaluates how significant formal remittance flows are to national economies by measuring their scale, economic impact and the size of the diaspora relative to the domestic population.

For Zimbabwe, analysts say remittances have evolved from supplementary household support into one of the economy’s central pillars.

International markets expert Munyaradzi Chiura said the ranking reflects how diaspora inflows continue to sustain economic activity despite recurring macroeconomic shocks.

“It reflects how well remittance flows capture their economic, social, and financial impact,” Chiura said, noting that transfers have strengthened financial inclusion through digital platforms and mobile money usage while cushioning households during periods of instability.

The latest ranking follows a record year for diaspora inflows. Remittances increased by about 14 percent in 2025 to an estimated US$2.45 billion, with the United Kingdom and South Africa remaining Zimbabwe’s largest remittance corridors.

Related Stories

These inflows now rival mining earnings and tobacco exports as one of the country’s main sources of foreign currency. Economists say their predictable nature has helped stabilise liquidity conditions, ease pressure on the exchange rate and support import financing in an economy frequently constrained by forex shortages.

Yet, despite the impressive volumes, financial sector experts warn that Zimbabwe is failing to convert remittances into productive capital capable of driving sustainable growth.

Financial technology systems and innovation specialist Jabulani Simplisio Chibaya argues that banks and financial institutions continue to treat remittances primarily as transactional income rather than developmental capital.

“The result is a missed national advantage,” Chibaya said. “Billions in inflows that could be powering SMEs, housing, and capital markets remain underleveraged. Until financial institutions rethink their role, from passive recipients to active enablers, we will continue to leave value on the table.”

Analysts describe the country’s remittance landscape as a paradox. On one hand, diaspora funds play a vital social role, financing food purchases, school fees, healthcare and daily consumption. This spending supports retailers and informal businesses while indirectly boosting tax revenues and circulating working capital across the economy.

On the other hand, the transition from consumption-driven transfers to investment-led financing remains limited. Economists argue that without targeted financial products — such as diaspora bonds, structured savings instruments or equity participation channels — Zimbabwe risks remaining highly dependent on remittances without fully unlocking their developmental potential.

Experts say the country’s top ranking should serve not only as recognition of diaspora resilience but also as a policy signal that deeper financial innovation is required to transform remittances from a survival mechanism into a sustainable engine of national growth.

Leave Comments