ZimNow Analysis Desk

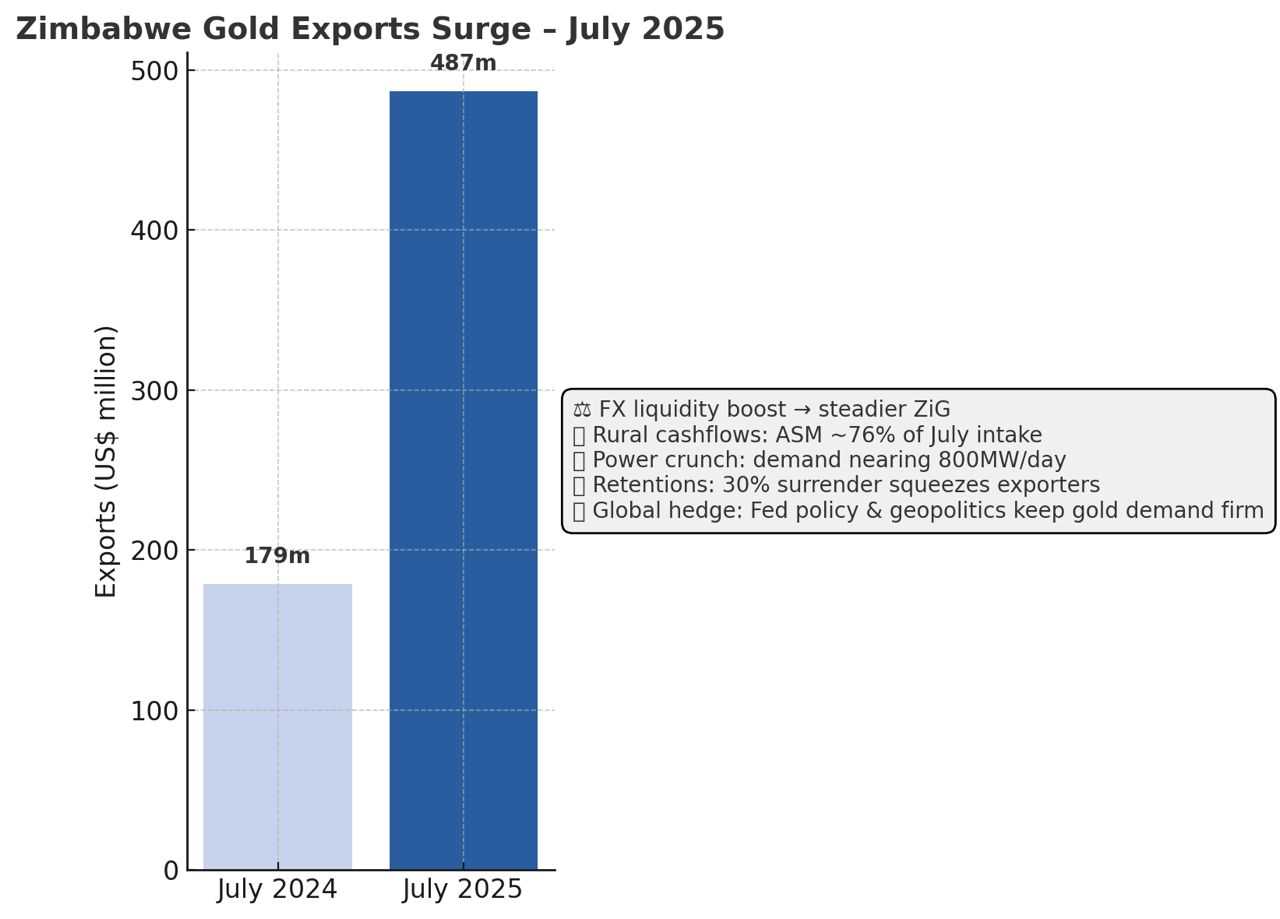

Zimbabwe earned US$487m from gold exports in July 2025—172% more than July 2024—taking Jan–Jul earnings to ~US$2.32bn as deliveries climbed 40.7% to 24,308 kg. Small-scale miners supplied the bulk of July’s 4.21 t.

Why now? (global tailwinds, local hustle)

• Prices + geopolitics: “Robust investment activity… underscores gold’s role as a hedge,” says Louise Street, Senior Markets Analyst, World Gold Council, after Q2 demand rose despite record-high prices.

• Exploration surge on the ground: “Frustrating for us, but… encouraging… this higher gold price has pulled the trigger on exploration,” says Craig Harvey, VP Technical Services, Caledonia Mining—with 24.3 t delivered in Jan–Jul (+40% y/y). Gold touched US$3,500/oz in April.

5 Fast Takeaways for Business

1. FX liquidity: More gold dollars usually mean smoother access to forex for importers via banks/auctions—RBZ notes reserves are now dominated by monetary gold, and it keeps intervening to meet “legitimate FX demand.”

2. Currency buffer: RBZ gold/FX reserves climbed (gold to 3.4 t by end-June), and it vows to keep building to anchor the ZiG. That helps price stability for fuel, meds, and spares—if inflows persist.

3. Supplier boom: July’s 4.21t intake was ~76% ASM—meaning rural cash flows into milling, transport, fuel, food, security, and services. (Small-scale miners delivered ~3.20t.)

4. Power + lead times: Growth strains lab capacity and electricity. Labs are “overwhelmed,” while miners flagged power needs rising toward 800 MW/day in 2025—budget for gensets/PPAs.

5. Surrender math: Exporters must surrender ~30% of forex (retention cut from 75% to 70% in 2025), supporting reserves but squeezing capex; plan working capital around it.

For “the unwashed masses” (plain talk)

• More gold dollars in → steadier ZiG → fewer sudden price spikes. RBZ says reserve cover is >100% and is still buying gold—not a magic wand, but it reduces volatility that hits groceries, transport, and school fees.

Related Stories

• Jobs and hustle money in mining towns: when ASM sells formally, cash circulates locally (shops, kombis, agro-inputs). July data shows ASM carried the month.

What could spoil the party (watch-outs)

• Power & costs: The Chamber of Mines warned costs are rising and energy demand is biting—profitability can still compress even with high prices.

• Bottlenecks: Lab/assay delays slow projects; clear SLAs with accredited labs and consider regional overflow options.

• Policy friction: The 30% surrender strains exporters’ USD cash flows; any further tweak changes project economics.

• Price risk: If global risk appetite swings or the Fed path surprises, gold can retrace; WGC notes H2 could trade in a narrower range unless shocks push it higher.

Quick actions for operators & suppliers

• Lock power: negotiate ZETDC load profiles/IPP wheeling where possible; budget diesel backup for Q4 rains. (COMZ flagged power as a 2025 crunch.)

• Speed the lab loop: pre-book assay slots, use a dual-lab strategy, and track turnaround as a KPI.

• Hedge the USD gap: map the 70% retention to payables; align deliveries to FX needs; use forward orders where viable.

• Go formal, get paid: FGR intakes are strong; formal channels improved pricing/settlement, pulling ASM into the net.

What to watch next (Aug–Sep)

• RBZ reserve updates & FX interventions (support for ZiG).

• Power tariffs/load-shedding guidance to miners.

• FGR monthly intake—can ASM keep >70% share?

• Global price drivers: U.S. data, Fed signaling, and new trade frictions.

Leave Comments